Beer Data Wars - Episode 4: Attack of 3 Tier Beverages

Attack of 3 Tier Beverages

Armed with the tools to compete, the craft rebels made significant advances in the retail universe throughout the second half of the last decade. The IPA Wars began to peak as the Dark Side pushed a number of disturbances through the force in the form of seltzers, spiked nostalgia, and flavored everything. A global pandemic took aim at the sanctity of beer data, firing a near fatal blow that sent rebel numbers off course for four challenging years. As the resistance regroups, their needs have become more sophisticated, requiring upgraded weapons and expert training. All the while, a rogue counsel of Jedi masters were plotting to fight at their side and restore growth to the galaxy.

The previous episode of Beer Data Wars focused on Armadillo Insights, a Tableau-based data visualization tool tailored for breweries eager to leverage market sales data. As pioneers in this niche, Armadillo reaped the benefits of early market leadership, a steep learning curve, and a sizable initial customer base. However, their success and subsequent mergers and acquisitions brought inevitable disruptions.

In 2020, 3 Tier Beverages entered the fray, founded by two former Armadillo users and ex-colleagues of mine, aiming to elevate the standards in the beverage alcohol data industry. As a latecomer, this Chicago-based startup avoided the initial costs of pioneering in an already established market and concentrated on differentiating itself. Their partnerships with NielsenIQ (NIQ) and Vermont Information Processing (VIP) brought together two of the most influential forces in beer data, focusing on service to fully realize their potential.

1. NIQ vs. Circana

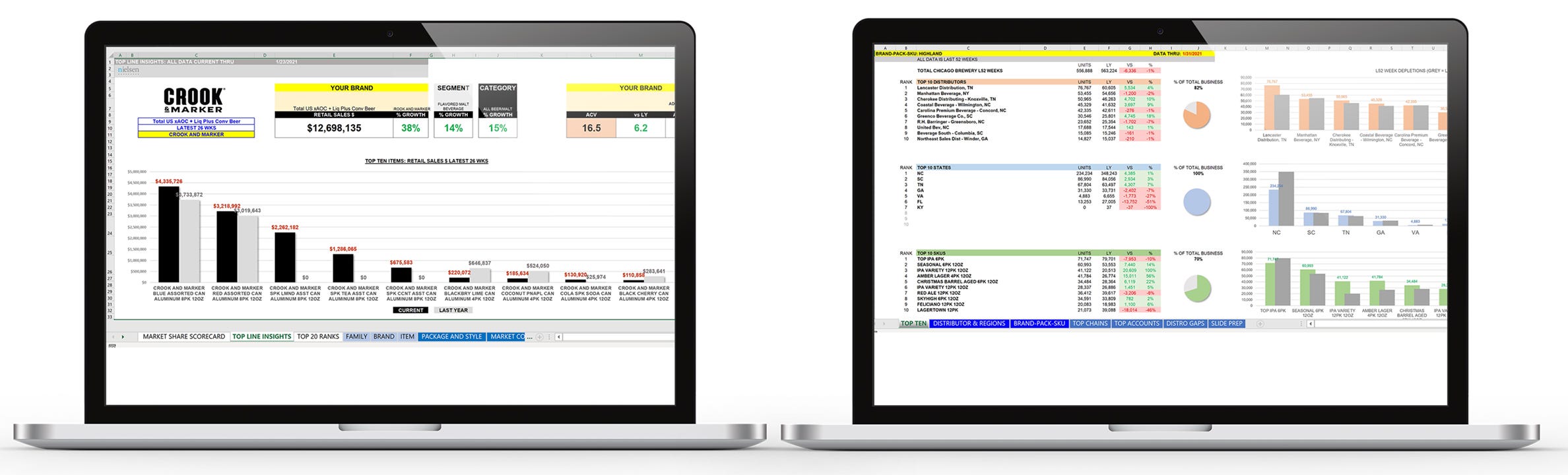

While Armadillo, powered by Circana (formerly known as IRI), allows users to query reports on demand, 3 Tier Beverages provides its clients with Microsoft Excel dashboards every four weeks, featuring the latest data drop from NIQ. As competitors, both NIQ and Circana strive to offer the most complete view of consumer trends, market dynamics, and the competitive landscape in the beverage alcohol industry. The quality of their data is a constantly moving target, with each company vying to establish new partnerships that best serve their customers' needs.

Not every major retailer is eager to share their data, which can result in coverage gaps. If some of a brewery's largest retail partners are absent from a dataset, market rankings might incorrectly portray them as weaker, potentially affecting their ability to secure future placements or promotions. Breweries should start by requesting data samples from both NIQ and Circana, then compare these to make an informed choice.

This comparison, along with discussions about the components and any significant missing elements, will highlight which dataset offers the most comprehensive insights for their specific regions. It's also crucial for breweries to research the strategic investments each company is making to broaden and enhance their understanding of retailer and consumer behavior. Having recently investigated NIQ, here are two examples of their recent investments:

Liquor Channel Expansion - Open State View: Just days ago, Nielsen announced an expanded and enhanced measurement of the Liquor Off-Premise Retail Channel, which has long been one of the most challenging to quantify with so many liquor chains and independent stores. Per their release, this advancement broadens the scope of store coverage by 2.8x for beer while providing a better understanding of the broad assortment of products that don’t necessarily reach other channels. In addition to a nationwide view, NIQ now is able to begin offering detailed views into the Liquor channel in 8 key states: California, Colorado, Florida, Maryland, Massachusetts, New Jersey, New York State, and Texas. Continued expansion of the Liquor channel views will be a game changer for NIQ.

On Premise Management (OPM): In 2022, NIQ acquired CGA to deliver insights into the locations where their clients’ brands are built, the on-premise. Regularly increasing coverage over this historic blindspot making up 61% of global beverage value sales (excluding wine) has put NIQ in a great position. Per their release earlier this month, OPM’s view continues to expand against a backdrop of changing on premise preferences, including a moderation in alcohol intake. Highlights of a recent study of 30,000 On Premise customers across 38 markets revealed the following highlights:

83% of global legal drinking age consumers have visited On Premise in the last 3 months, with 62% visiting weekly

Visitation has remained stable globally, despite most consumers feeling financially worse off than they were last year.

On Premise plays a vital role in facilitating connections with friends and loved ones, with 3 of the fastest growing reasons for visit being – Connecting with family and friends, to celebrate and to have fun.

Although visits are stable, global On Premise sales of beer, malt beverages and cider volume sales have fallen by 4.0% in the last 12 months. Spirits have fallen by 7.6%.

Gen Z and younger Millennials (to age 34) are most likely to increase their visits to On Premise over the next 3 months with a net increase of 27% vs 14% for all On Premise visitors.

Even though consumer visits to the On Premise remain high, consumers’ relationship with alcohol is mixed, with more than a third (37%) of consumers now drinking less alcohol than they were 12 months ago.

Source: NIQ Press Release - July 11,2024

Vermont Information Processing (VIP)

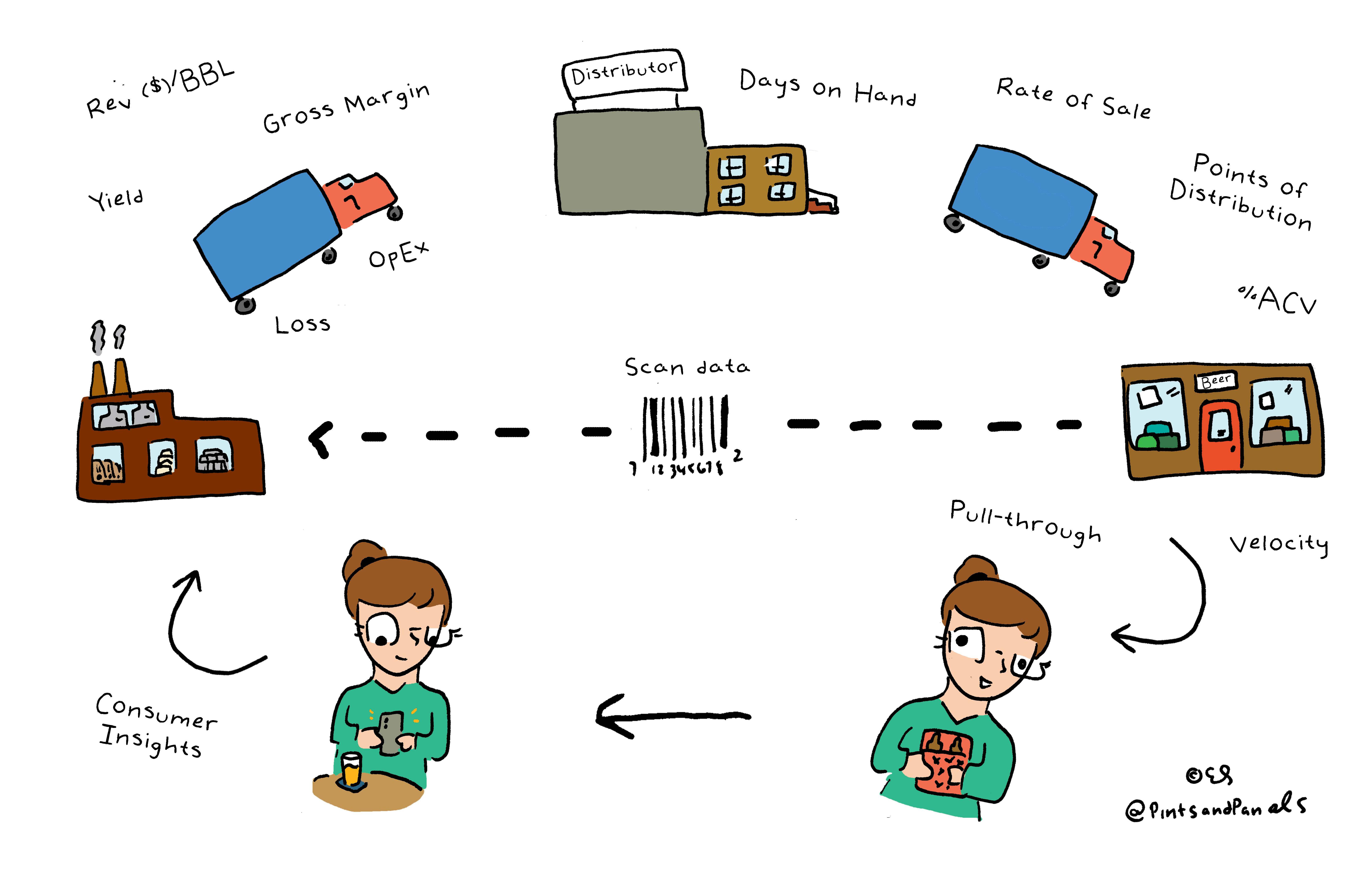

While shipments to distributors represent true sales for a brewery in their financials and scans complete the transaction to the end customer, there’s arguably no more important piece of data to a brewery’s analysis than it’s depletions. These sales from their distributors to retailers provide the perfect hybrid to measuring a product’s health and combined with its rate-of-sale (ie Avg Cases Sold Per Week), informs the brewery of when to brew their next batch, while keeping freshness optimal.

VIP has dominated the depletion data landscape for as long as I’ve worked in this industry. As the ERP system of choice for beer distributors around the country, they have the keys to the depletion data kingdom. A tool called iDig using their data is sold back to brewery suppliers to provide insights into their distributor’s sales and inventory levels to help plan. Partnerships between NIQ, VIP, and 3 Tier Beverages allow the fantasy of depletions being presented alongside scan data to become a reality, both in iDig and as part of their dashboards. Still though, great data, delivery methods, and presentation are only as effective as the individuals dedicated to putting them into action.

The Sales Analyst

For every craft brewery where distribution plays a significant role in their business model, the Sales Analyst is an indispensable position that too few organizations utilize. I affectionately refer to them as the "central command center" for the sales team because they centralize the analysis necessary to determine:

Where sales team members can allocate their time most effectively,

What information and selling stories to equip them with, and

How to condense and visualize that data into simple, impactful presentations.

Having one or more individuals dedicated to these areas allows the field sales team to focus more on their strengths, including relationship building. While it might seem like an obvious advantage, the return on investment isn't always immediate. The combination of data analysis, visualization, and strategic skills is prevalent in many industries, but it's rarer in the beer industry, especially among craft breweries, which often lack the scale to justify the expense.

Hiring the first ever sales analyst in an organization is a bet that could take 6, 9, or 12 months or more to bear its fruit, depending on the circumstances. Not every brewery has the cash flexibility to afford this level of investment, nor the time and skillsets to effectively onboard and integrate the position into the team. Since the average brewery can afford somewhere between zero and one sales analyst, that means there’s no redundancy. In the event of turnover, the brewery is back to square one.

3 Tier Beverages took these challenges into account when building out their model and team, making the sales analyst skillset one of their optional service offerings. Breweries concerned that they don’t have a full job’s worth of 40 hours/week of analysis are offered a flexible solution with the ability to outsource their sales analyst, and even prove the concept to their organization with an aim to hire the position down the road. Since 3T has over 250 supplier partners in bev-alc, they’re able to provide a well-rounded perspective and identify with any brewery’s situation.

Learning to master tools like NIQ, VIP, or their competitors is a significant time commitment that often requires mentorship from experienced leaders, akin to Jedi training. These investments are a priority for suppliers eager to compete in the deepest echelons of the industry. However, for the thousands of small brewers focused exclusively on their local markets, there's a need for more niche, specific, and consumer-centric data. An intriguing arsenal of such data has been stockpiled and is being deployed by Next Glass’ Untappd Insights, which has generously provided Beer Crunchers with full access to dig up insights for you all.

Coming up next in Episode 5…

Thank you for reading and supporting Beer Crunchers. Here’s a note I’ve prepared for you to Copy+Paste, then send to your boss 😎

Hey [Insert Your Boss’ Name] - I get inspiration for new ideas and important perspective by reading Beer Crunchers’ blog. They recently launched a premium tier with additional insider-only content to help make these posts continue to happen, at an increased frequency, and with the hope of bringing in new contributors by the end of the year. While $199.99 is not a small amount of money, over the course of an entire year it really only takes one big takeaway to put this investment into the black for me. Given how much I get out of reading Beer Crunchers, could I expense a premium subscription?